How Fintech is transforming the financial sector and what it means for policymaking.

Policymakers around the globe expect technology-driven innovation in finance (Fintech) to spur financial inclusion and competition and hence economic development at scale. Technology and financial services, the World Bank suggests, are powerful growth sectors and growth enablers for Arab economies.

The Fintech sector in the MENA region has been growing since 2012. Countries like the UAE have started to put enabling policies in place and venture funding for Fintech has remarkably picked up with USD 237 million in 181 deals since 2015, finds the Mena Fintech Venture Investment report. As of 2019, there were more than 330 Fintech providers, as CGAP reports, predominantly in payments and mostly startups in the seed and early-growth stages.

The digitalization in finance evidently transforms markets and institutions at unprecedented pace with sweeping consequences for the development of financial systems worldwide.[1]

The Financial Inclusion for the Arab Region Initiative (FIARI) empowers policymakers and regulators in making safe financial systems work inclusively for Arab societies. The exchange reveals more about the state of play in the digital financial transformation in the region.

How is the sector changing and what does it mean for policymaking? Overall, 5 fundamental trends can be observed.

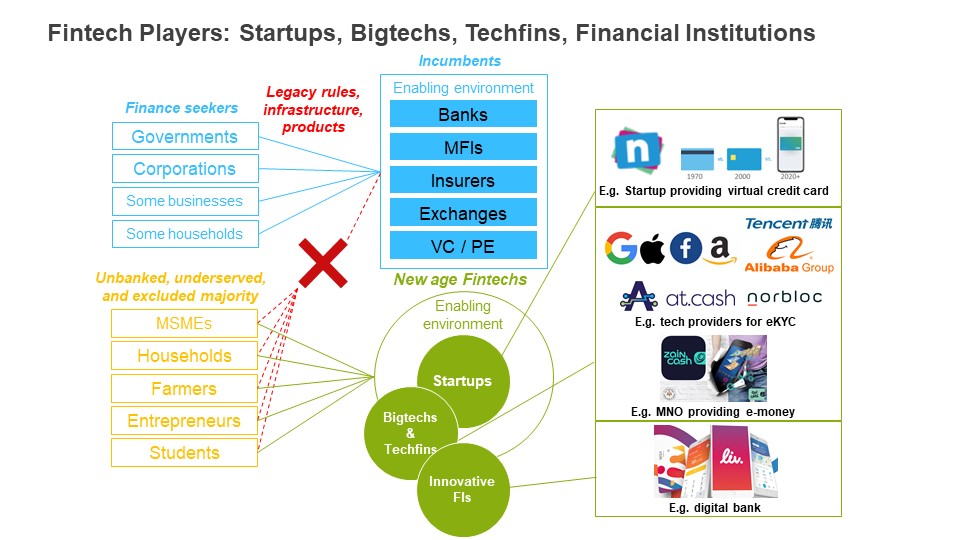

I. The type of players in finance are changing, and they can fall outside the traditional regulatory perimeter. Disruptive startups, technology firms (Bigtechs and Techfins) as well as innovative financial institutions come into play to use the possibilities of the latest wave of technologies. They are drawn by opportunities such as the record-level of remittances running on legacy rails, the vast market potential of around 63% of unbanked people in the Arab countries according to World Bank, or the massive funding gap in businesses of around USD 200 billion as estimated by IFC Enterprise Studies.

Technology seeks scale to be profitable and the new players benefit from different unit economics compared to legacy financial institutions. Startups harness asset-light, less regulated, partly outsourced business models. Bigtechs capitalize on their vast data pools from their core business in telco, IT, commerce or entertainment and on network effects in their platforms. They innovate, cross-sell or on-sell financial services that are customized to the individual, cheaper and more convenient – hence the potential for financial inclusion. Yet, the growing number of players and their business model, channel, or product innovations trigger discussions around the scope and effectiveness of the regulatory architecture in place to safeguard financial stability, protection, and integrity.

II. Traditionally segregated sectors are converging, requiring cooperation and better inter-institutional coordination among authorities. Incentivized by growth or efficiency gains, Fintech innovations emerge in the areas of customer on-boarding, payments and transfers, lending, investments and savings, at government level, in monetary policy or supervisory and regulatory practice. The application of artificial intelligence, big data analytics, cloud solutions, or blockchain in finance drives the convergence of the technology (ICT) and financial services sectors. The role of the ‘ecosystem’ takes centre stage. Policymaking and regulation for fintech spans across jurisdictions, including prudential and non-prudential financial supervision, competition, data privacy, ICT and cybersecurity, requiring a coordinated approach at the national level.

III. The rate of innovation and the volume of data are increasing, requiring more attention and regulatory resources at least in the short term. More digital services hit the market. More users adopt them. The volume, velocity, and variety of available data as a valuable resource increase, while risks generally grow with the concentration of data. That is why Bigtechs can distort competition and outsourcing becomes a concern for cybersecurity. The data abundance can affect the system and burden oversight resources. On the one hand, this calls for modern frameworks regulating the protection and the availability of (big) data (like open banking/API initiatives e.g. in Bahrain). On the other hand, regulatory technology can help to prop up compliance, real-time monitoring and market analytics, allowing regulators to take their mandate for secure, sound financial systems to the next level.

IV. The scope of financial policy objectives is changing, which adds to the duties of authorities. Policymakers in more and more countries promote Fintech sectors in an attempt to enhance competition, financial inclusion or, beyond that, job creation. Governments deploy Fintech in public services. Officials rush to study the use of next-gen technology in their monetary policy (e.g. digital currencies). With the Fintech ecosystem, the political pressure grows. The roles and responsibilities of financial policymakers and regulators tend to shift.

V. The regulatory tools – or regulatory innovations – for enablement and supervision are transforming. Alongside regulations, regulators have more varied tools available that they can put to use in a facilitative role to enable responsible Fintech. Regulatory innovations can include innovation hubs and regulatory sandboxes (like in Bahrain, Jordan, Egypt, or UAE), alongside Suptech, all of which have implications on institutional settings and market developments. Overall, capacity building, cooperation, and novel regulatory approaches have become decisive.

In the MENA region, the Fintech sector is growing at 30% CAGR, indicates a Milken Institute report. Growing VC funding, rapidly expanding mobile and internet connectivity, and the young and increasingly tech-savvy population will further propel growth over the next years.

Amidst these developments, central bankers and other officials from Morocco, Tunisia, Egypt, Jordan, Palestine, and Iraq recently joined the first of its kind FIARI Innovation Lab.

In this week-long peer exchange and study programme, carried out by GIZ on behalf of BMZ as part of the Initiative, the regulators particularly addressed cutting-edge issues such as open banking and alternative credit scoring, regulatory innovations, and home-grown policy solutions to promote Fintech for inclusion. Hosted in the region’s Fintech hubs of Abu Dhabi and Dubai, the group studied the local authorities’ approaches to Fintech regulation. By meeting up with the Fintech accelerators of both hubs, the central bankers have gotten to know the innovative business models of a total of twenty Fintech startups. The discussions revealed the need for corridors to allow Fintech firms to passport and scale across borders more easily which builds on common framework conditions.

In joining the Innovation Lab, central bankers from across the region decided to take action in leading innovation topics in their organizations and driving forward the transformation of ecosystems for safe Fintech, in times of drastic changes.

By Atilla Kaiser-Yücel

Any views expressed are those of the author and not necessarily of the author’s organization.

[1] References

AFI (2018). Fintech for Financial Inclusion: A Framework for Digital Financial Transformation. Available at: https://www.afi-global.org/sites/default/files/publications/2018-09/AFI_Fintech_Special%20Report_AW_digital.pdf

Arner, Barberis, Buckley, Zetzsche (2017a). Regulating a Revolution From Regulatory Sandboxes to Smart Regulation. Available at: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3018534

Arner, Barberis, Buckley, Zetzsche (2017b). Fintech and RegTech: Enabling Innovation While Preserving Stability. Available at: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3211708

Arner, Barberis, Buckley, Zetzsche (2017c). From Fintech to TechFin. The Regulatory Challenge of Data-driven Finance. Available at: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2959925

Arner, Barberis, Buckley (2016). Fintech, RegTech and the Reconceptualization of Financial Regulation. Available at: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2847806

BCBS (2018). Implications of fintech developments for banks and bank supervisors, Bank for International Settlements. Available at: https://www.bis.org/bcbs/publ/d431.pdf

BIS (2019). Big tech in finance: opportunities and risks. Available at: https://www.bis.org/publ/arpdf/ar2019e3.pdf

FSB (2019). Fintech and Market Structure in Financial Services. Market developments and potential financial stability implications. Available at: https://www.fsb.org/wp-content/uploads/P140219.pdf

FSB (2017). Financial Stability Implications from Fintech. Supervisory and Regulatory Issues that Merit Authorities’ Attention. Available at: https://www.fsb.org/wp-content/uploads/R270617.pdf

IMF / World Bank (2019). Fintech: The Experience So Far. Available at: https://www.imf.org/en/Publications/Policy-Papers/Issues/2019/06/27/Fintech-The-Experience-So-Far-47056

World Bank (2018). The Bali Fintech Agenda: A Blueprint for Successfully Harnessing Fintech’s Opportunities. Available at: http://documents.worldbank.org/curated/en/390701539097118625/pdf/130563-BR-PUBLIC-on-10-11-18-2-30-AM-BFA-2018-Sep-Bali-Fintech-Agenda-Board-Paper.pdf