Our partners in the Central Banking community increasingly pay attention to sovereign digital currency – partners with whom we share long-standing relationships in all matters concerning financial systems for the public good. And the public is going to witness probably the most fundamental leap in the evolution of money since the invention of credit cards half a century ago and of bank notes over a millennium ago. Here is how.

The subject of the debate is Central Bank Digital Currency, in short CBDC (or GovCoin).

Minting and issuing money in the form of coins and bank notes is the business of Central Banks. Technically, a CBDC is sovereign digital money and it qualifies as virtual store of value, means of payment and unit of account. Simply put, it is the digital form of the cash in your pocket.

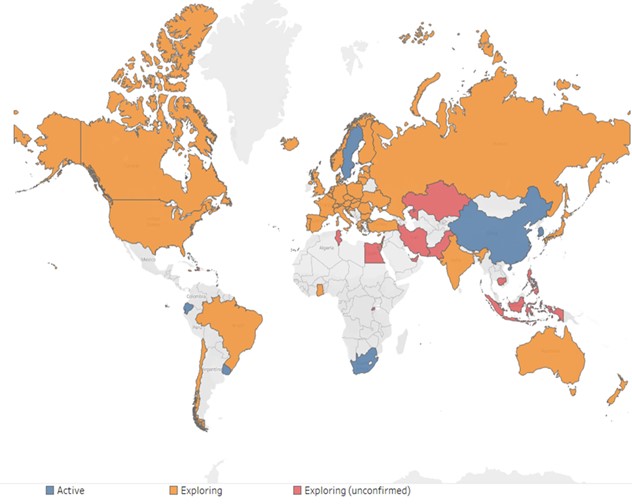

The Bahamas were first to launch a CBDC, the Sand Dollar. The Eastern Caribbean, the Marshall Islands, and Jamaica are set to follow. China with the Digital Yuan and Sweden with the e-Krona are the two most advanced countries among the big economies that prepare for a sovereign digital currency. Most of the work is still conceptual. However, Central Banks representing a fifth of the world’s population are said to be expecting the issuance of such sovereign digital currency in the coming three years, according to global surveys by the BIS.

Image: Central banks are at various stages of developing sovereign digital currency

Source: the IMF; also check out Bloomberg.

At the centre of this innovation are incumbents: monetary authorities. In contrast, new players in the currency space – which is traditionally a public domain – would be global stablecoins such as Facebook’s Diem and crypto-assets of the Bitcoin sort, neither of which however are officially (fiat) money.

The motivations for issuance of CBDC vary across countries, as do the policy approaches and technical designs. Let us walk through an example CBDC model by examining the core elements of who would be the users, what would be the key value proposition, and how value would be generated.

Who: the users

The sovereign digital currency could be available for use by the general public. The target group of such a retail CBDC hence includes, but is not limited to, all citizens, foreign residents, visitors, businesses and corporations.

Use could initially be confined to domestic borders but, following analysis, development of standards, pilots, and payments system integration, could be widened to international use, for example, for cross-border payments in commerce and remittances.

Financial institutions and financial services providers would play a distinct role in the distribution and handling of CBDC, which most likely would initially be rolled out as an extension to cash, not a replacement thereof.

What: the value proposition

One can argue that cash (banknotes and coins) creates a platform which lets people and businesses trade goods and services with one another: mutual trust is based on the sovereign issuer’s credibility since money has no intrinsic value. A sovereign digital currency creates a digital platform which lets the entire population take advantage of digital possibilities – theoretically without discrimination.

- First, because it is legal tender by definition, i.e. it can be exchanged anywhere, CBDC generates network effects by default: anyone would use this digital money as it becomes a standard for everyone. This could boost the ecosystem for digital finance.

- Second, because it is backed by the Central Bank, i.e. a liability of the Bank, the sovereign digital currency would be a risk-free alternative to other means of payment and particularly to the latest, untested innovations such as stablecoins or crypto-assets.

- Third, this type of digital money is basically free of charge and provides an economically cheaper alternative in accessing and using a safe store of value and modern means of payment for anyone and everyone, especially the financially underserved: in most countries these are the majority of the population including in the informal economy and vulnerable groups.

- Fourth, because it comes with modern infrastructure, a CBDC can provide the efficient railways on top of which a host of other added value services can be offered to users by the private sector or by Governments such as for benefits, conditional stimulus (hot money), or relief in times of crises.

For example, countries that had invested into the digital financial infrastructure before the COVID-19 pandemic and crisis were able to better distribute needed funds. With CBDC, many countries could leapfrog in making modern day, efficient payments available to the public.

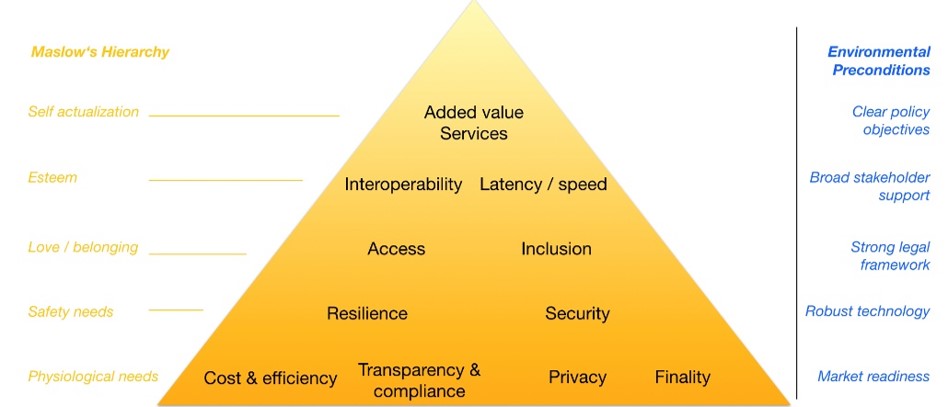

Value to digital money users could unfold in multiple ways. The value proposition can be derived from the needs that a CBDC must meet to be successful.

Image: Pyramid of Central Bank Digital Currency Needs

Source: own illustration based on interviews; hierarchy for illustration purposes; right column FED Reserve.

How: value creation and capture

Firstly, the value creation here in this example involves a two-tier, token-based retail CBDC run on a permissioned decentralized ledger: the sovereign digital currency would be distributed and handled through financial institutions and financial service providers which serve as interface to users.

The Central Bank would mint and issue digital money as a token which could be stored in, send from and received in wallets, say, provided by qualified providers. The underlying infrastructure and protocol could, but does not necessarily have to, be based on a distributed ledger that is governed by the Central Bank.

Remember that the essential features in this sovereign digital currency, the CBDC, makes it fundamentally different from the Bitcoin-like crypto-assets and global stablecoins: technologically, legally, and economically.

The so created digital money could allow to capture social, ecological, and financial (cost saving) value, for example:

- Financial inclusion: enabling the population and economy to benefit from access to digital financial services, which can lead to socio-economic and productivity gains

- Financial system stability: greater control over payment system security and efficiency

- Monetary sovereignty and precision: greater effectiveness in terms of policy rates and money supply

- Digital economy: new impetus from digital financial architecture for innovation in the economy

- Carbon footprint: reduction of carbon emissions from minting, issuance, collection of cash

- Crisis resilience: greater resilience of financial system in times of natural disasters

Yet, more research and tests will be needed to provide evidence.

The debate in the community and our analyses show us that there are yet many unknowns around CBDC design that merit attention and global cooperation (with potentially more unknowns that have not even crossed our minds yet).

For example, how do you make sure that such digital currency can be used like cash by everyone and anonymously, while still having sufficient controls to avoid misuse by perpetrators for illicit purposes? Europeans value privacy for a future Digital Euro a lot. Possible solutions are starting to emerge.

The financial inclusion is indeed a strong motive by Central Banks for a general public CBDC and much more a motive in emerging markets and developing economies.

The CBDC topic is more and more keeping the Central Banking community busy, including from the Levante, over the Gulf to the Maghreb. Numerous expert consultations and even decision trees have seen the light of the day, as we curate a body of knowledge in our network.

As members pay this much time and effort to understanding global developments, prospects, and implications, we stand by to establish ties and facilitate cooperation across borders to put CBDC for the public good to the test.

By Atilla Yücel